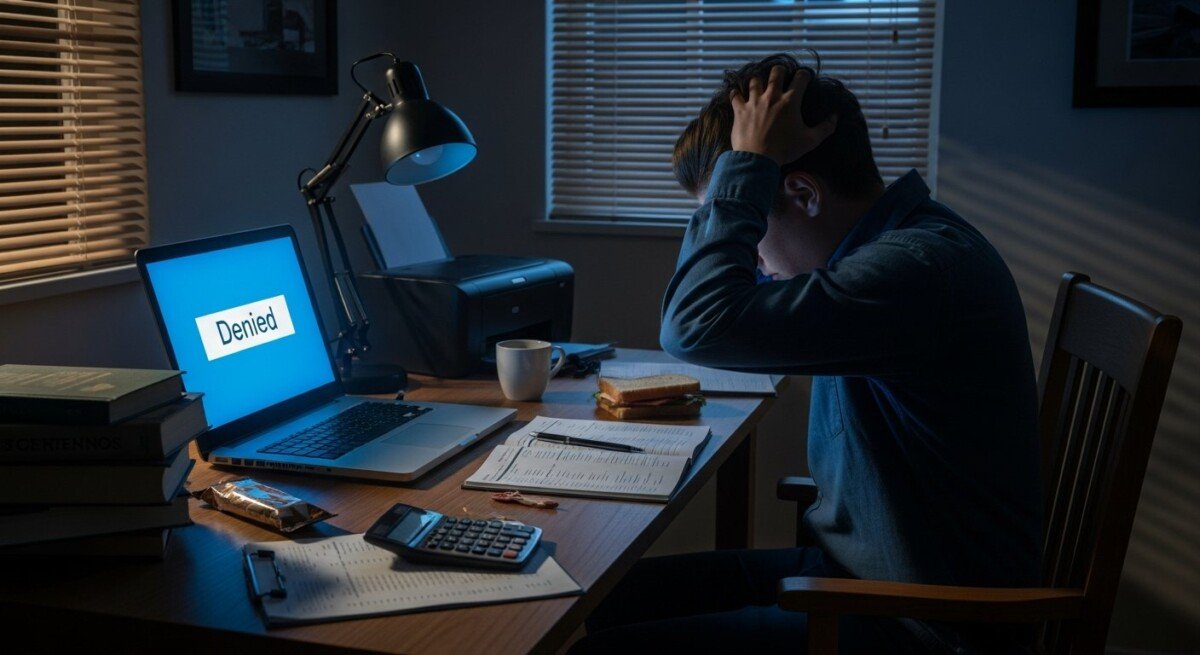

What Happens If Your Cash Advance Application Is Denied

A denied cash advance application requires specific steps. Learn what happens next and how to explore better financial alternatives.

By Julia Anderson

You’ve submitted an application for a cash advance, hoping for a quick financial lifeline. The wait for a decision can be stressful, and receiving a denial notice can feel like a significant setback. It’s a common situation, but one that leaves many borrowers wondering about the immediate consequences and their next steps. Understanding what happens if your advance cash application is denied is crucial for managing your financial health and planning your path forward. A denial is not the end of the road, it’s a signal to pause, assess, and strategize. This guide will walk you through the typical aftermath of a denial, the reasons behind it, and the actionable steps you can take to recover and potentially secure the funding you need through other means.

Immediate Aftermath and Understanding the Denial

When you receive notification that your application has been denied, the first thing to do is remain calm and avoid panic-driven decisions. The lender is legally required to provide you with an adverse action notice, typically via mail or email. This notice is your key to understanding the “why” behind the decision. It must specify the primary reasons for the denial, which could range from issues with your credit report to inconsistencies in your application information. Do not discard this notice, it is an essential document for your next steps.

Common reasons for a cash advance denial include a low credit score, a high debt-to-income ratio, insufficient or unverifiable income, recent overdrafts or bounced checks on your bank account, or simply not meeting the lender’s specific age or residency requirements. Sometimes, the issue is not with you but with the application itself, incomplete forms or mismatched personal details can trigger an automatic rejection. It’s important to review the adverse action notice carefully. If the denial cites information from a credit report, the notice will include the name, address, and phone number of the credit bureau that supplied the report. You have the right to request a free copy of that report within 60 days to check for errors that may have influenced the decision.

Your First Steps After a Denial

Once you have the denial notice in hand, a systematic approach will serve you better than a scattered one. Your immediate actions should focus on information gathering and damage control. First, obtain your free credit report from the bureau mentioned in the notice. Scrutinize it for inaccuracies, such as accounts you didn’t open, incorrect payment statuses, or outdated negative items. Disputing errors with the credit bureau can improve your score and help future applications.

Second, contact the lender directly. While they are not obligated to reverse their decision, a polite inquiry can sometimes provide more nuanced details than the formal notice. Ask if there is any additional documentation you could provide to reconsider the application, or if they can clarify a specific reason. This conversation can also reveal if you were denied for a product you didn’t qualify for but might be eligible for a different one, though you should be cautious about immediately applying for another product with the same lender. Finally, take a hard look at your financial snapshot. A denial is a clear indicator that your current financial profile, as presented, does not meet certain risk criteria. This is a moment for honest budgeting. For a deeper dive into evaluating your readiness for this type of product, consider reviewing our resource on key considerations before taking a cash advance.

Strategic Alternatives to Explore

A denied application forces you to broaden your perspective. Several alternative paths may be available, some of which might offer better terms than the original cash advance you sought. It is vital to explore these options methodically rather than applying for every loan you see, as multiple hard inquiries in a short period can further damage your credit score.

Consider the following avenues, ranked generally from most to least preferable from a cost and risk perspective:

- Negotiate with Current Creditors: Contact companies you already owe money to (utility providers, landlords, credit card companies) and explain your temporary hardship. Many have hardship programs that can allow for a delayed or reduced payment.

- Seek a Secured Loan or Credit-Builder Loan: These products, often available through credit unions, use collateral or a locked savings account to mitigate the lender’s risk, making approval more likely for those with poor or thin credit.

- Explore a Payday Alternative Loan (PAL): Offered exclusively by federal credit unions, PALs have strict caps on interest and fees, providing a much safer short-term borrowing option if you qualify for membership.

- Utilize a Side Hustle or Gig Work: Generating immediate income through freelance platforms, selling unused items, or taking on temporary work can cover your need without creating debt.

- Request a Salary Advance: Some employers offer non-loan advances on earned wages. This is a fee-free way to access money you’ve already earned.

Rushing into another high-cost product should be your last resort. For a comprehensive look at other possibilities, our article on viable alternatives to a cash advance outlines several strategies for maintaining financial health.

Repairing Your Profile for Future Success

The denial is a data point in your larger financial journey. Use it as motivation to build a stronger foundation so that future applications, for credit products or otherwise, are more likely to succeed. This process is not instantaneous, but consistent effort yields results. Start by addressing the specific reason for your denial. If it was a low credit score, develop a plan to improve it. This always begins with making all current minimum payments on time, every time. Payment history is the single largest factor in most credit scoring models.

Next, work on reducing your overall credit utilization, which is the percentage of your available credit limits you are using. Paying down revolving debt, like credit cards, is the most effective method. If you have older accounts in good standing, keep them open, as a longer credit history generally helps your score. You should also avoid applying for new credit frequently. Each application typically results in a hard inquiry, which can temporarily lower your score. Space out your credit applications by at least six months when possible. Building an emergency savings fund, even if it starts with just a few dollars per week, can prevent the need for emergency borrowing in the future. For borrowers in specific states, understanding local regulations and options is also key, as detailed in our guide to navigating advance cash services in Pennsylvania.

Frequently Asked Questions (FAQs)

Does a denied cash advance application hurt my credit score?

The application itself may result in a hard inquiry, which can slightly lower your score for a short period. The denial itself is not reported to credit bureaus and does not directly impact your score. However, multiple applications and denials in a short timeframe can compound the negative effect of the hard inquiries.

How long should I wait before applying for another loan after a denial?

It is advisable to wait at least 30 to 90 days. Use this time to address the reasons for the denial, such as paying down debts or correcting errors on your credit report. Applying again immediately without any change in your circumstances will likely lead to another denial and further credit score damage.

Can I apply with a different lender right away?

Technically, yes, but it is often a poor strategy. Different lenders have similar eligibility criteria. A denial from one is a strong signal that others will also see you as high-risk. It’s better to understand and fix the underlying issue first.

What if the denial was due to an error on my credit report?

You have the right to dispute inaccurate information with both the credit bureau and the company that provided the data (the “furnisher”). The Fair Credit Reporting Act (FCRA) requires them to investigate, typically within 30 days. If the information is corrected, you can ask the lender to reconsider your application with the updated report.

Should I use a loan broker or “bad credit” lender after a denial?

Exercise extreme caution. While some legitimate lenders specialize in working with borrowers with poor credit, this space is also rife with predatory lenders and scams. Research any company thoroughly, check for state licensing, and read all terms and conditions. Exorbitant fees and opaque terms are major red flags.

Facing a denied cash advance application can be discouraging, but it is a manageable financial event. The critical response is to shift from seeking a quick fix to engaging in strategic financial management. By thoroughly understanding the reasons for the denial, exploring safer and more sustainable alternatives, and taking concrete steps to improve your financial profile, you turn a short-term rejection into a long-term gain. Your financial stability is built not on a single approved loan, but on the habits and knowledge you develop over time. Let this experience inform a stronger, more resilient approach to managing your money and credit.