Understanding Payday Loans: A Quick Overview

Payday loans, often referred to as short-term, high-interest loans, are designed to provide immediate financial relief to individuals facing urgent monetary needs. These payday loans in new Orleans are typically due on the borrower’s next payday, hence the name. In New Orleans, payday loans have become a popular option for those who require quick access to cash without the lengthy approval processes associated with traditional bank loans.

However, it is crucial for borrowers to understand the terms and conditions, as these loans often come with high interest rates and fees that can lead to a cycle of debt if not managed properly. In the vibrant city of New Orleans, payday loans are accessible through various lenders, both online and in physical locations.

These loans are particularly appealing to individuals with poor credit scores, as they do not require a credit check. However, the convenience of payday loans in New Orleans comes with significant financial risks. Borrowers are advised to carefully assess their repayment capabilities before committing to such loans, as failure to repay on time can result in additional fees and increased financial strain. Understanding the implications of payday loans is essential for making informed financial decisions and avoiding potential pitfalls.

The Legal Landscape of Payday Loans in New Orleans

The legal landscape surrounding payday loans in New Orleans is shaped by both state and federal regulations designed to protect consumers while allowing lenders to operate within defined boundaries. In Louisiana, payday loans are governed by the Louisiana Deferred Presentment and Small Loan Act, which sets forth specific guidelines regarding loan amounts, fees, and repayment terms.

Under this legislation, payday loans in New Orleans can be issued for amounts up to $350, with a maximum loan term of 30 days. The law also caps the finance charge at 16.75% of the loan amount, ensuring that borrowers are not subjected to exorbitant interest rates. Additionally, lenders are required to be licensed by the state, which helps maintain a level of oversight and accountability.

Despite these regulations, the payday loan industry in New Orleans has faced criticism for its impact on financially vulnerable individuals. Critics argue that the high fees and short repayment periods can lead to a cycle of debt, where borrowers are forced to take out new loans to cover old ones. In response to these concerns, some consumer advocacy groups have called for stricter regulations, such as capping the number of loans a borrower can take out in a year or extending the repayment period to reduce the financial burden on borrowers. Nevertheless, payday loans in New Orleans remain a popular option for those in need of quick cash, highlighting the ongoing debate between consumer protection and access to credit.

How Payday Loans Work: A Step-by-Step Guide

Payday loans in New Orleans operate as short-term financial solutions designed to provide immediate cash to individuals facing urgent monetary needs. The process begins with the borrower selecting a reputable payday loan provider, either through a physical storefront or an online platform. Once a lender is chosen, the borrower is required to complete an application form, which typically necessitates the provision of personal identification, proof of income, and a valid bank account. Upon submission, the lender evaluates the application, often approving it within minutes if the borrower meets the necessary criteria. This swift approval process is one of the defining characteristics of payday loans, making them an attractive option for those in need of quick funds.

After approval, the borrower receives the loan amount, which is usually a percentage of their upcoming paycheck, directly deposited into their bank account. The repayment terms are straightforward, with the full loan amount plus any applicable fees and interest due on the borrower’s next payday. This repayment is often automatically deducted from the borrower’s bank account, ensuring a seamless transaction. However, it is crucial for borrowers to fully understand the terms and conditions, as failure to repay the loan on time can result in additional fees and potentially impact their credit score. In New Orleans, as in other locations, payday loans serve as a critical financial tool for many, but they require careful consideration and responsible management.

Pros and Cons of Payday Loans in New Orleans

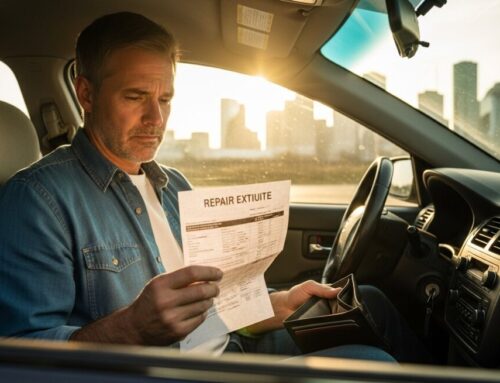

Payday loans in New Orleans offer a quick and accessible solution for individuals facing urgent financial needs. One of the primary advantages of these loans is their accessibility, as they are available to individuals with varying credit histories. This feature makes payday loans particularly appealing to those who may not qualify for traditional bank loans due to poor credit scores. Additionally, the application process for payday loans is typically straightforward and fast, often providing funds within a day. This rapid turnaround can be crucial for borrowers who need immediate cash to cover unexpected expenses such as medical bills or car repairs.

However, there are significant drawbacks to consider when opting for payday loans in New Orleans. The most notable disadvantage is the high interest rates and fees associated with these loans, which can lead to a cycle of debt if not managed carefully. Borrowers may find themselves needing to take out additional loans to cover the costs of previous ones, exacerbating their financial situation. Furthermore, the short repayment terms, often due within two weeks, can be challenging for individuals who are already struggling financially. It is essential for potential borrowers to weigh these pros and cons carefully and consider alternative financial solutions before committing to a payday loan.

Alternatives to Payday Loans: Exploring Other Options

When considering financial solutions, it is crucial to explore alternatives to payday loans, especially in areas like New Orleans where these loans are prevalent. Payday loans in New Orleans, while offering quick cash, often come with high interest rates and fees that can lead to a cycle of debt. Instead, individuals might consider options such as personal loans from credit unions, which typically offer lower interest rates and more manageable repayment terms. Additionally, many credit unions provide financial counseling services to help borrowers better manage their finances and avoid future financial pitfalls. Another viable alternative is seeking assistance from local non-profit organizations that offer financial aid and support.

These organizations often provide emergency funds or low-interest loans to those in need, helping to alleviate the immediate financial burden without the high costs associated with payday loans in New Orleans. Furthermore, budgeting and financial planning services offered by these organizations can empower individuals to make informed financial decisions, ultimately reducing the reliance on high-cost borrowing solutions. By exploring these alternatives, individuals can find more sustainable financial solutions that support long-term financial health. Exploring these alternatives can lead to more sustainable financial health and stability.

The Impact of Payday Loans on New Orleans Communities

Payday loans in New Orleans have become a significant financial tool for many residents, particularly those facing unexpected expenses or short-term cash flow issues. These loans, characterized by their high-interest rates and short repayment periods, are often marketed as a quick solution for financial emergencies. However, their impact on the community is multifaceted. On one hand, payday loans provide immediate financial relief to individuals who may not have access to traditional banking services or credit options. This accessibility can be crucial for those living paycheck to paycheck, offering a temporary respite from financial stress.

On the other hand, the prevalence of payday loans in New Orleans has raised concerns about their long-term effects on borrowers and the broader community. Critics argue that the high costs associated with these loans can lead to a cycle of debt, where borrowers are forced to take out additional loans to cover previous ones, thereby exacerbating financial instability. This cycle can have ripple effects, contributing to economic disparities and financial insecurity within the community. Moreover, the concentration of payday loan establishments in economically disadvantaged areas has sparked debates about the ethical implications of targeting vulnerable populations. As such, while payday loans offer immediate solutions, their broader impact on New Orleans communities necessitates careful consideration and regulation.

Tips for Choosing a Reputable Payday Loan Provider

When seeking payday loans in New Orleans, it is crucial to choose a reputable provider to ensure a secure and beneficial borrowing experience. Start by researching potential lenders thoroughly. Look for companies with a strong track record and positive customer reviews. Checking for accreditation with the Better Business Bureau (BBB) can also provide insight into the lender’s reliability and customer service standards. Additionally, ensure that the lender is licensed to operate in Louisiana, as this compliance is a key indicator of their legitimacy and adherence to state regulations. Another important consideration is the transparency of the loan terms.

A reputable payday loan provider will clearly outline the interest rates, fees, and repayment schedule before you commit to the loan. Avoid lenders who are vague about these details or who pressure you into signing agreements without adequate explanation. It is also advisable to compare offers from multiple lenders to find the most favorable terms. By taking these steps, you can make an informed decision and select a payday loan provider in New Orleans that meets your financial needs while safeguarding your interests. Remember, responsible borrowing is key to managing payday loans effectively.

Managing Payday Loan Debt: Strategies for Borrowers

Managing payday loan debt can be a daunting task, especially for borrowers in New Orleans who may find themselves caught in a cycle of short-term borrowing. To effectively manage payday loans in New Orleans, it is crucial to first understand the terms and conditions of the loan, including interest rates and repayment schedules.

Borrowers should prioritize creating a detailed budget that accounts for all monthly expenses and income, allowing them to allocate funds specifically for loan repayment. This proactive approach not only helps in meeting payment deadlines but also prevents the accumulation of additional fees and interest, which can exacerbate financial strain. Another effective strategy for managing payday loan debt is to explore alternative financial solutions that may offer more favorable terms.

Borrowers in New Orleans can consider options such as credit counseling services, which provide guidance on debt management and financial planning. Additionally, consolidating multiple payday loans into a single loan with a lower interest rate can simplify repayment and reduce overall debt. Engaging with local community resources and financial advisors can also provide valuable insights and support, helping borrowers to navigate their financial challenges more effectively. By implementing these strategies, individuals can regain control over their finances and work towards achieving long-term financial stability.

Future Trends: The Evolution of Payday Loans in New Orleans

The landscape of payday loans in New Orleans is poised for significant transformation as both regulatory changes and technological advancements reshape the industry. With increasing scrutiny from federal and state authorities, lenders are expected to adopt more transparent practices, ensuring that borrowers are fully informed about the terms and conditions of their loans.

This shift towards greater transparency is likely to foster a more competitive market, where lenders strive to offer more favorable terms to attract discerning consumers. Additionally, the integration of digital platforms is anticipated to streamline the application process, making it more accessible and efficient for potential borrowers. As a result, the future of payday loans in New Orleans may see a shift towards more responsible lending practices that prioritize consumer protection and financial literacy.

Technological innovations are set to play a pivotal role in the evolution of payday loans in New Orleans. The adoption of artificial intelligence and machine learning algorithms can enhance the assessment of a borrower’s creditworthiness, allowing lenders to offer more personalized loan products. This technological shift not only improves the accuracy of risk assessments but also reduces the time required for loan approvals, providing a more seamless experience for borrowers.

Furthermore, the rise of mobile banking and digital wallets is expected to facilitate easier repayment options, thereby reducing the likelihood of borrowers falling into a cycle of debt. As these trends continue to unfold, the payday loan industry in New Orleans is likely to become more integrated with the broader financial ecosystem, offering consumers more flexible and sustainable financial solutions.

Explore our website, AdvanceCash, to apply for a loan, or contact our customer service team today to learn more about how we can assist you.

About Alex Thompson

Related Posts